This is a case concerning the undue influence of an 80-year old lady by a much younger man, whom she believed at the time was her boyfriend, in respect to the transfer of her house. The Probate Bureau was contacted by Ms. Dawn Moursi, the daughter of the elderly lady, Ann Gurney, to discuss reclaiming her rightful inheritance. During the initial meeting, Ms. Moursi spoke with David West, Managing Director at The Probate Bureau.

Probate Solicitors Case Studies

We have advised and helped literally thousands of people with probate, wills and trusts over the years, so we understand better than most that the legislation surrounding probate, inheritance tax and the recent Care Bill can be daunting and difficult to understand for a lot of people.

Our clients often find it hard to make sense of all that legislation spouted at them from various quarters and end up feeling confused and frustrated. It should be the aim of all legal and financial practitioners to avoid this situation and make sure their clients fully understand the process and work being undertaken on their behalf.

One of the best ways we have found of explaining both the probate process and some of the additional work that can be completed to suit their individual needs is by using case studies.

Here are some some real case studies we've undertaken. We have changed the names to aliases in order to protect clients' privacy and hope that the examples we've listed may strike a chord and help you appreciate that our primary aim is to help people and make a difference:

Probate Bureau Help Daughter Reclaim Estate

Solving A Case Of Sibling Rivalry

The Probate Bureau was contacted by brothers Robert and Dennis Ashkettle following the death of their mother, a Mrs Louisa Ann Ashkettle. In the 1986 Will, Mrs. Ashlettle’s estate was left to Robert, Dennis and Rosalind in equal shares. In the 1999 Will, however, the estate was left to Rosalind alone. This case focuses on testamentary capacity and want of knowledge and approval, notwithstanding that it had been prepared and its execution supervised by a solicitor.

Heir Trace Probate

Who was to inherit a Hoarder's £1.8m estate? A few years ago we were presented with an interesting case which required the utilisation of all our skills and expertise; from heir tracing, probate administration, house clearance and investment of an inheritance into trust. It all started when we received a call from a nursing home stating a resident had died leaving no next of kin. We took up the challenge and 12 weeks later via Western Australia we located a legitimate beneficiary; in Stevenage...

Trust Case Study

The Estates of the late Eric and Joanna Anderson The Probate Bureau was appointed by Mrs Anderson to deal with her late husband's estate after his death in December 2008. Whilst his estate was ongoing, in September 2009 her daughter also died unexpectedly. The Probate Bureau was able to bring an amazing degree of expertise into play to solve a potentially complex and expensive outcome

Contested Will Case

Mother and son argue over £1m estate. Mrs Jones (not her real name), was in dispute with her son Stuart over her brother’s £1m estate. Her brother had died with a Will leaving his estate to Stuart (just one of Mrs Jones’s three children). The deceased had made a prior Will, made many years before, which left his estate to Mrs Jones whose intention it would have been to then leave it equally between her three children, Stuart receiving one third. Her view was that Stuart had hijacked the whole estate…

Probate Case Study

The Estate of the late Alfred Jones We recently administered probate for the Alfred Jones estate. Mr Jones died leaving only an elderly wife who under the terms of his Will was the sole beneficiary of his estate. Mrs Jones stood to inherit around £20,000 as well as their £215,000 property held in Mr Jones' sole name. We visited Mrs Jones to discuss the estate with her and provide free probate advice.

Request callback

We recieved your callback request. Will be contact you soon

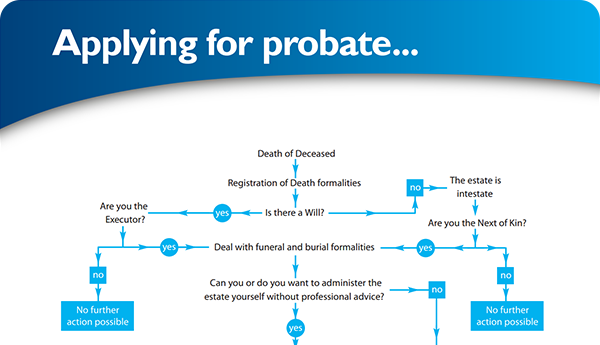

×Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×