10 Legal Ways to Reduce Inheritance Tax in the UK (2026 Guide)

")

10 Legal Ways to Reduce Inheritance Tax in the UK (2026 Guide)

Introduction

Inheritance tax, often called IHT, has become one of the most significant financial concerns for families in the UK. Rising property values combined with frozen tax thresholds mean more estates than ever are crossing the IHT threshold. Yet inheritance tax is frequently described as the “voluntary tax”, because with careful planning, a substantial amount of it can be reduced or avoided entirely.

Many families fail to take advantage of the legal reliefs available simply because they do not understand the rules or assume inheritance tax is unavoidable. Others delay planning until it is too late, leaving their loved ones with a larger tax bill than necessary. With the right advice and a proactive approach, it is possible to preserve more of your estate and ensure your assets pass smoothly to the next generation.

At The Probate Bureau, we specialise in inheritance tax mitigation and estate planning. This detailed 2026 guide sets out ten legitimate, HMRC-compliant strategies that can significantly lower your potential inheritance tax liability. Each method is fully legal, widely used, and appropriate for individuals and families of all estate sizes. Whether you are planning for the distant future or arranging your finances now, these approaches can help reduce tax, protect wealth and ensure your estate is handled exactly as you intend.

1. Use Your Annual Gifting Allowance

Every individual in the UK is entitled to give away up to £3,000 per tax year without these gifts being added back into their estate for inheritance tax purposes. This is known as the annual gifting exemption. If you do not use this allowance, it can be carried forward for one tax year, meaning a couple could give away up to £12,000 if neither used their previous year’s allowance.

Although £3,000 may not seem significant, regular use of this exemption over many years can reduce the size of an estate by tens of thousands of pounds. The primary advantage is that these gifts fall immediately outside of your estate, so they do not trigger the seven-year rule that applies to larger gifts.

For families who want to transfer wealth gradually and support children or grandchildren during their lifetime, this allowance is one of the simplest and most effective tools available. Many people use the exemption to help with school fees, university costs, deposits for first homes, or day-to-day support.

The key to making this exemption effective is consistency. Regular gifting ensures that more wealth is transferred during your lifetime, helping reduce the taxable value of your estate over many years.

2. Make Small Gifts Throughout the Year

In addition to the £3,000 annual exemption, HMRC also allows individuals to make unlimited small gifts of up to £250 per person per tax year. These gifts must go to different individuals, and they cannot be combined with another exemption for the same recipient.

Although £250 may seem modest, small gifts to several family members each year provide a straightforward way to reduce your estate value while offering practical support to loved ones. For grandparents, this exemption is particularly useful for birthday and Christmas gifts. Over time, small gifts accumulate and can significantly reduce your taxable estate.

The small-gift allowance is often overlooked but is a valuable tool for gradual, tax-free estate reduction. It is fully exempt from inheritance tax immediately, requires no complex documentation, and is simple to administer.

3. Take Advantage of Wedding or Civil Partnership Gifts

Wedding and civil partnership gifts receive special tax treatment under UK law. Provided the gift is made before the ceremony and the marriage or partnership actually takes place, the following exemptions apply:

- Up to £5,000 can be given tax-free to your child.

- Up to £2,500 to a grandchild or great-grandchild.

- Up to £1,000 to anyone else entering into a marriage or civil partnership.

These exemptions allow families to support newlyweds financially at an important stage of life while reducing the size of the donor’s estate. The amounts are per donor, meaning a couple can double the available exemption for the same recipient.

Wedding gift exemptions are immediately effective and do not fall under the seven-year rule. For families looking to support younger generations with buying a home, building savings or starting a family, these exemptions provide a tax-efficient way to contribute.

4. Make Regular Gifts from Surplus Income

Regular gifts out of surplus income are one of the most powerful inheritance tax planning tools available and are often misunderstood or underused. HMRC allows individuals to make ongoing gifts from excess income that are immediately exempt from inheritance tax, provided strict conditions are met.

To qualify, these gifts must come from income, not capital. They must also form part of a regular pattern, such as monthly transfers, annual school fee payments, or ongoing contributions to savings accounts. In addition, the gifts must not reduce the donor’s standard of living.

The advantage of this exemption is significant. Unlike larger gifts that fall under the seven-year rule, gifts from surplus income are exempt immediately. They do not require waiting periods and do not count towards the nil-rate band.

To ensure HMRC recognises these gifts as exempt, proper documentation is essential. Maintaining bank statements, letters of intent and written records demonstrating the regular nature of the gifts is important. At The Probate Bureau, we help clients document these gifts effectively so they are fully compliant with HMRC expectations.

For high-income individuals who may not need all of their monthly or annual income, this is one of the most tax-efficient strategies available.

5. Leave Assets to Your Spouse or Civil Partner

Transfers of assets between spouses or civil partners are entirely exempt from inheritance tax, regardless of the amount involved. This is one of the most generous tax reliefs available and forms a cornerstone of most estate plans.

If your estate is below the nil-rate band threshold at the time of death, any unused portion of your allowance can be transferred to your surviving spouse. This effectively doubles the available exemption for the couple. In 2026, this means a couple can pass up to £650,000 tax-free through the nil-rate band alone.

This relief also applies to assets passing through a will or held jointly. It ensures that the surviving spouse is not burdened with tax immediately after their partner’s death.

Although leaving everything to your spouse delays inheritance tax rather than eliminating it outright, it provides an opportunity to plan ahead as a couple. By the time the second spouse dies, additional strategies may have been used to reduce the estate value further.

6. Use the Residence Nil-Rate Band (RNRB)

The Residence Nil-Rate Band was introduced to help families pass on the family home to direct descendants. In 2026, it allows an additional £175,000 tax-free allowance per person, on top of the standard nil-rate band.

When combined with the transferable allowance between spouses, this means a married couple could potentially leave £1 million to their children or grandchildren free from inheritance tax.

To qualify, the property must be the main residence, and it must be left to direct descendants. The allowance is reduced for estates worth more than £2 million, which makes early planning essential for high-value estates.

The RNRB is complex and requires careful structuring of assets and wills. At The Probate Bureau, we help families maximise their entitlement and avoid losing the benefit through unintentional reductions or poor estate distribution.

7. Use Trusts to Protect Wealth for Future Generations

Trusts remain one of the most effective ways to manage, protect and pass on assets while reducing inheritance tax exposure. They allow you to transfer assets out of your estate while retaining a degree of control over how and when they are used.

There are many types of trusts, including Bare Trusts, Discretionary Trusts and Interest in Possession Trusts. Each has different tax implications, rules and benefits. Trusts can help ensure that young beneficiaries do not receive large sums before they are ready, protect vulnerable family members and prevent assets from being lost through divorce or financial mismanagement.

Trusts are particularly useful for families with significant assets who want to avoid repeated inheritance tax on the same money. Instead of wealth passing in full to each generation and being taxed again at 40 percent, a trust can preserve assets across multiple generations.

At The Probate Bureau, we collaborate with specialist solicitors to ensure trusts are established correctly, fully comply with HMRC rules and reflect your long-term intentions.

8. Leave Money to Charity

Charitable giving is not only rewarding but also tax-efficient. Gifts to registered charities are completely exempt from inheritance tax. This means that every pound donated reduces the taxable value of your estate.

Furthermore, if at least 10 percent of your net estate is left to charity, the inheritance tax rate applied to the remaining estate reduces from 40 percent to 36 percent. This reduction can create substantial tax savings while benefiting causes you care deeply about.

Charitable legacies can take many forms, including fixed monetary gifts, percentage gifts, or charitable trusts. Whether you wish to leave a small proportion of your estate or a significant legacy, charitable gifts are a meaningful way to support your values while reducing your family’s tax burden.

9. Protect Your Pension Pot

Pensions are one of the most inheritance tax-efficient assets available. In most cases, they sit outside your estate, meaning they are not subject to inheritance tax when you die.

If you die before age 75, your pension can usually be passed to your beneficiaries tax-free. If you die after age 75, beneficiaries pay tax at their marginal income tax rate, which can be significantly lower than the 40 percent inheritance tax rate.

This makes pensions a powerful tool for long-term estate planning. Rather than drawing pension funds early or spending from pension assets first, many people choose to preserve their pension and draw income from other taxable assets instead. This strategy leaves more inheritance tax-free value available for their beneficiaries.

It is important to complete a nomination or expression of wishes form with your pension provider to ensure your pension passes to the correct individuals. Without this, distribution may follow default rules rather than your chosen instructions.

10. Use Life Insurance to Cover Inheritance Tax Liabilities

Even with extensive planning, some estates will remain liable to inheritance tax. A life insurance policy written in trust can provide a simple and effective solution. When written in trust, the policy payout is kept outside of your estate, meaning it is not subject to inheritance tax.

The funds pay directly to the trust, giving your beneficiaries immediate access to money that can be used to settle the inheritance tax bill. This prevents the need to sell property, shares or other assets quickly at an unfavourable time. It provides certainty, liquidity and peace of mind.

Life insurance for IHT planning is particularly valuable for owners of high-value estates, business assets or illiquid property portfolios. The Probate Bureau regularly works with clients to structure these policies correctly and ensure they meet HMRC requirements for trust status.

Professional Guidance for 2026 and Beyond

Inheritance tax is an area where rules change regularly, thresholds rarely adjust and personal circumstances vary widely. Seeking professional advice can make a significant difference to the tax liability faced by your estate.

At The Probate Bureau, we offer comprehensive inheritance tax planning services tailored to individual and family requirements. These include:

- Detailed estate reviews.

- Lifetime gifting strategies.

- Trust creation and management.

- Collaboration with solicitors and financial advisers.

- Long-term planning for multi-generational wealth.

- Ongoing support for annual gifting and estate changes.

With thoughtful planning, your estate can benefit from the full range of available reliefs and exemptions.

Conclusion

Reducing inheritance tax is not about avoiding obligations. It is about ensuring that your hard-earned wealth benefits the people and causes you care about rather than being lost unnecessarily to tax. By taking action early and following legitimate HMRC-approved strategies, you can protect your family’s financial future and pass on more of your estate.

The Probate Bureau offers expert guidance to help you navigate inheritance tax with clarity and confidence. To discuss your personal situation and explore the best strategies for your estate, contact us for a free, no-obligation consultation.

Back To BlogShare This Post

Recent posts

- Probate Delays and How to Speed Things Up in 2026 By Admin , 03/02/2026

- Inheritance Tax Planning: 2026 Allowances and Exemptions Guide By Admin , 03/02/2026

- Making a Will at Christmas: Why the Holidays Are the Right Time By Admin , 23/12/2025

2015 Archive

2016 Archive

2018 Archive

2019 Archive

2020 Archive

0 Archive

- December 2 posts

2023 Archive

- July 10 posts

2026 Archive

- February 13 posts

Blog Categories

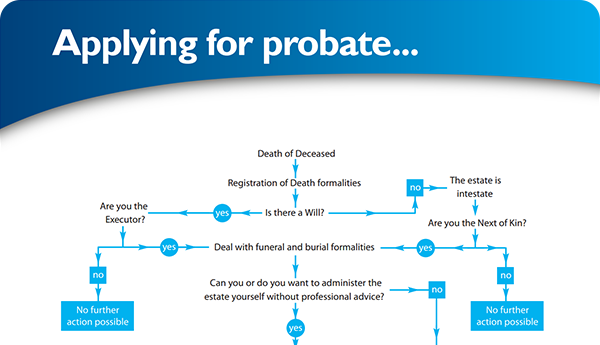

Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×