What Happens to a Mortgage After Death?

Losing someone is hard enough without a letter from the mortgage lender landing on the doormat. Yet for many families, one of the first money worries after a death is the home and the loan still secured against it.

If you are an executor or a surviving partner, you may be wondering who is now responsible for the mortgage repayments, and whether the property is at risk. This guide explains what happens to a mortgage after death UK families can expect, step by step and in plain English.

What happens to a mortgage after death UK homeowners should know

A mortgage does not disappear when the borrower dies. The mortgage debt stays attached to the property and becomes part of the estate, along with any outstanding debts the person left behind. The way a mortgage after death UK lenders deal with the balance depends mainly on how the loan was held, either in one name or jointly with someone else.

Until the estate is settled, the lender still expects the monthly payments to be met. Knowing the position early matters, and it helps to understand how much probate costs, so the family can budget for the months ahead.

Sole-name mortgages

When the mortgage was in the deceased person's name alone, responsibility passes to the deceased's estate rather than to any one person. The executor uses estate funds, or the proceeds of a sale, to repay the outstanding mortgage. If there is a will, the executor manages this. Under intestacy rules, where there is no will, an administrator takes on the role. Our executor checklist for 2026 sets out those duties clearly.

Joint mortgages

Most couples own their home under a joint tenancy. Here, when a partner dies, the survivor can automatically inherit the whole property, and the surviving spouse or civil partner then takes on the joint tenancy mortgage. The mortgage provider will usually want to confirm that the survivor can afford the payments alone, and may ask for a remortgage or a new mortgage, where shopping around can sometimes find a better deal.

Does a mortgage get frozen when someone dies?

You may be asking whether the mortgage is frozen when a person dies. In most cases it is not. Interest continues to build and payments remain due, although many lenders will pause enforcement action for a short grace period, sometimes offering a payment holiday, while the estate is assessed. It helps to contact the lender quickly, send a copy of the death certificate, explain the situation, and ask what breathing space they can offer. Who pays the mortgage during probate?

Probate is the legal process of dealing with someone's estate. While it runs, the mortgage still needs servicing. Payments can come from the deceased's bank accounts, from savings, or from beneficiaries who want to protect the property. If money is tight, the executor should speak to the lender about a temporary arrangement rather than let arrears grow. You can see typical timings in our guide on how long probate takes.

Who pays the mortgage during probate?

Probate is the legal process of dealing with someone's estate. While the probate process runs, the mortgage still needs servicing. Payments can come from the accounts the deceased held as account holder, from savings, or from beneficiaries who use their own funds to protect the property. If money is tight, the executor should speak to the lender about a temporary arrangement rather than let arrears grow. You can see typical timings in our guide on how long probate takes.

What if the estate cannot repay the mortgage?

Sometimes the estate has insufficient funds to clear the balance and simply does not hold enough money. A mortgage after death UK estates cannot cover is usually dealt with through the sale of the property first. If the home is worth more than the loan, selling it repays the outstanding balance and often leaves something for the beneficiaries.

If the property is in negative equity, meaning the mortgage is larger than its value and the person who died owes money beyond what the home is worth, there may not be enough in the estate to pay the lender, leaving an insolvent estate. In that case the lender can only claim against the estate, not against the family personally. Beneficiaries do not inherit the remaining debt, although they may lose the asset. Early advice keeps these decisions calm and informed.

A mortgage is rarely the only money owed. Alongside it, the deceased may have left other debts such as credit card debt, personal loans and car finance. These unsecured debts usually rank behind secured debts like the mortgage, so the personal representative settles all the debts in the correct order from the estate before anything passes to beneficiaries. It is worth checking each credit agreement, as some are written off automatically on death.

Life insurance and clearing the balance

Many homeowners take out life insurance or a decreasing term policy alongside the mortgage. When the borrower dies, this pays out and can clear some or all of the loan. Checking whether such a policy exists is one of the first practical steps in dealing with a mortgage after death UK households often forget to make.

If a policy covers the full balance, the property can pass to beneficiaries free of the loan. If it only covers part, the estate makes up the difference. Our financial services team can help you review cover, pensions, and other assets tied to the estate.

Your options for the property

Once the position is clear, the family usually has three main routes to consider.

| Option | What it involves | Best suited to |

|---|---|---|

| Keep and take over | A surviving owner or beneficiary continues the payments, often after a remortgage. | Joint owners or heirs who can afford the loan. |

| Sell the property | The estate sells the home and repays the lender from the sale proceeds. | Estates where no one can or wants to keep the home. |

| Transfer with the debt | A beneficiary inherits the property and the outstanding mortgage together. | Heirs who are happy to take on the balance. |

The right choice depends on affordability, the size of the estate, and any inheritance tax due. Valuing the estate correctly, including debts, is a legal duty, and GOV.UK explains how to value an estate. For a wider view of money matters after a bereavement, MoneyHelper offers useful, impartial guidance.

Getting help with a mortgage after death UK families can trust

Sorting a mortgage after death UK executors often face can feel overwhelming, especially alongside grief and other paperwork. You do not have to work it out alone. Our fixed-fee probate administration service handles the estate from start to finish, so you always know the next step and exactly what it will cost.

We are a local Hertfordshire team based in Ware, and we explain everything in plain English, from wills and lasting powers of attorney through to full estate administration. If you would rather talk it through first, our friendly team is glad to help. Speak to us about a fixed price before you commit to anything.

Frequently Asked Questions

Can I inherit a house that still has a mortgage?

Yes. You can inherit a property along with its outstanding mortgage. You will usually need to take over the payments, remortgage in your own name, or sell the home to repay the lender.

Do the mortgage payments have to be made straight away?

Payments remain due after death, but most lenders allow a short grace period. Contact them early to explain the situation and agree a temporary plan while the estate is being sorted.

What happens if there is no life insurance to cover the loan?

The loan is repaid from the rest of the estate, usually from the sale of the property or other assets. If the estate cannot cover it in full, the lender claims what it can, and beneficiaries are not personally liable for any shortfall.

Can the lender repossess the property during probate?

Repossession is rare while an estate is being administered and the payments are kept up. Problems tend to arise only if payments stop and no one keeps the lender informed, so early contact matters. Our probate administration team can manage this for you.

Talk to The Probate Bureau

Every estate is different, so the sooner you have clear advice, the easier the next steps become. Learn more about the way we work on our homepage, or get in touch with The Probate Bureau today for clear, fixed-fee guidance on probate, wills, and estate administration.

Back To BlogShare This Post

Recent posts

- Selling House Probate UK: Complete Guide By , 16/07/2026

- What Happens to a Mortgage After Death? By , 16/07/2026

- What Are the Duties of an Executor? By , 15/06/2026

2015 Archive

2016 Archive

2018 Archive

2019 Archive

2020 Archive

2026 Archive

2023 Archive

- July 12 posts

0 Archive

- December 1 posts

Blog Categories

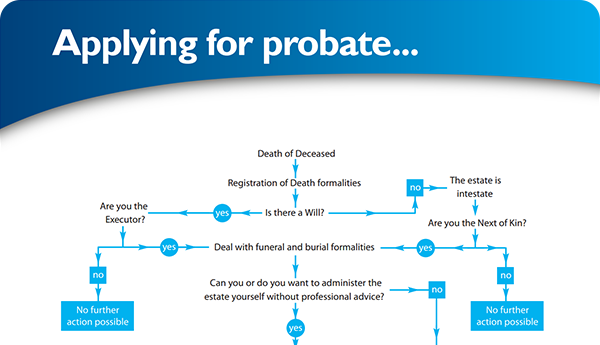

Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×